posted 14th March 2024

Mergers and acquisitions (M&A) are increasingly pivotal for large corporations and agile, dynamic SMEs navigating competitive sectors. These strategies offer vital avenues for growth, diversification, and sustainability in the rapidly evolving business landscape. The mid-term and long-term trends influencing the M&A market are complex, mirroring the multifaceted and opportunistic nature of the current economic environment.

In H2 2023, despite the challenges of rising interest rates, inflation, and geopolitical tensions, the UK and Ireland's mid-market sectors showed remarkable activity. This resilience was notably propelled by the strategic initiatives of SMEs, underscoring the significance and adaptability of M&A approaches in facing the future's uncertainties.

Most recently, GS Verde Group was pleased to have been ranked in the Top 3 of the UK and Ireland M&A Mandate League Table for Q4 2023, published by Dealsuite. This followed closely on the Group's ranking as the most active legal adviser and corporate finance adviser in Wales on Experian's Market IQ full-year report for 2023, the only adviser to feature in both categories.

Unveiling market confidence in uncertain times

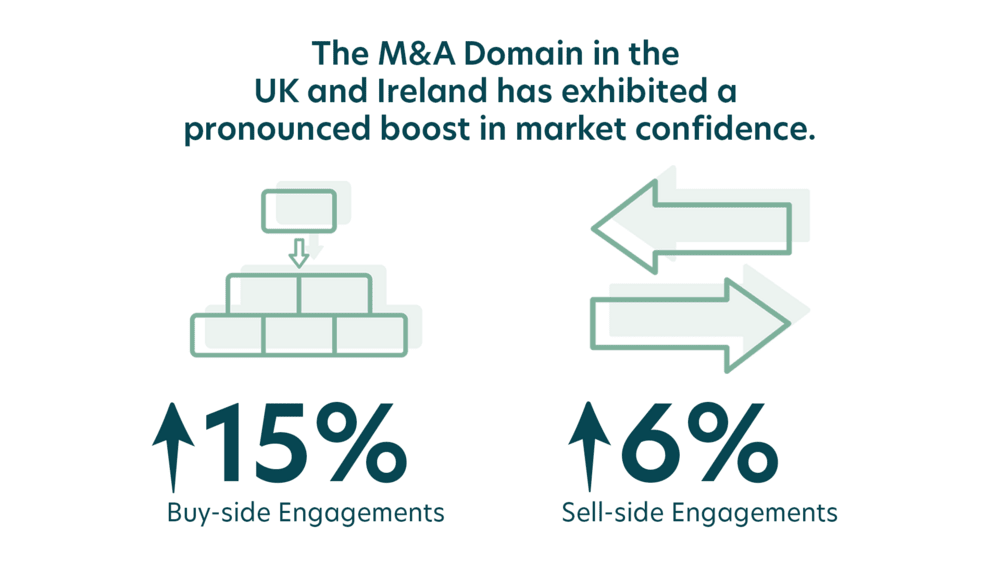

In a climate of economic uncertainty, the M&A domain in the UK and Ireland has exhibited a pronounced boost in market confidence, highlighted by a significant uptick in both buy-and sell-side transactions. This period witnessed a 15% increase in buy-side engagements and a 6% rise on the sell-side, demonstrating businesses' unwavering optimism and proactive approach toward seizing growth and consolidation opportunities.

In terms of valuation, the average EBITDA multiple within the mid-market sphere of the UK and Ireland's M&A scene remained consistent at 5.1x, with slight variations across different sectors. In the latter half of the year, the wholesale trade sector notably outperformed the retail sector. The wholesale trade sector achieved a higher average EBITDA multiple of 3.9x while the retail sector had 3.5x, marking a departure from the previously identical averages in H1 2023.

Insights into market-driving sectors

The evolution of sector dynamics vividly illustrates the changing landscape of the market. Business services continued to dominate in terms of transaction volumes, representing 20% of market activities and achieving an average EBITDA multiple of 5.2x - affirming its integral role in the economic framework.

Meanwhile, the IT sector expanded its transactional share from 11% to 14% with an average EBITDA multiple of 7.6x. The sector also demonstrated the greatest variability in multiples, reflecting its price volatility tied to technological risks.

Similarly, the healthcare sector's transaction share grew from 5% to 9%, and boasted an average EBITDA multiple of 7.8x, underscoring the escalating significance of digital transformation and healthcare innovation. These developments in specific sectors offer insights into the strategic priorities and investment interests currently driving the market.

The scale effect: the impact of small firm premium on SME transactions

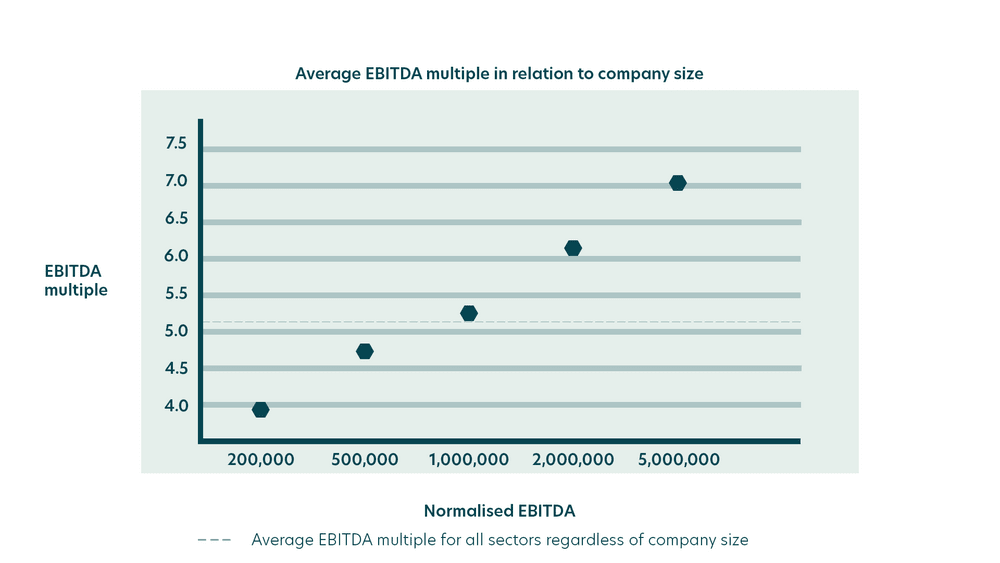

In 2021, researchers delved into the "Small Firm Premium" phenomenon affecting EBITDA multiples for SMEs across the UK, specifically targeting firms with EBITDA ranging from £200,000 to £5,000,000. This bracket is representative of the typical scale of SMEs in the UK and Ireland, mirroring their operational size. The investigation showed that smaller entities encounter elevated risk premiums due to dependencies on customers, or suppliers, and the risk of losing technical expertise. These factors collectively depress their valuation multiples relative to their larger counterparts. The disparity in EBITDA multiples at the lower and upper ends of this spectrum is noteworthy, clearly demonstrating the significant influence of firm size on their market valuation.

Corroborating these findings, the Dealsuite M&A Monitor is in harmony with the latest data, showcasing a significant rise in SME market activities - particularly among businesses with EBITDA below £5 million. These now constitute 62% of the market's transactions, a considerable increase from 48% in the first half of 2023.

On the other hand, it emphasises the profound effect of company size on transaction multiples. Smaller firms, grappling with higher risk premiums and operational interdependencies typically secure lower EBITDA multiples compared to larger counterparts. This trend demonstrates the critical importance of risk assessment and its influence on valuation decisions in the mid-market sector.

Unlocking cross-border potential in interconnected markets

Cross-border transactions reveal an expanding market appetite for opportunities beyond national confines. Dealsuite's comparative analysis of EBITDA multiples across various regions, including the UK & Ireland, DACH region (with an average EBITDA of 5.5x), France (average EBITDA of 5.3x), and the Netherlands (average EBITDA of 4.75x), showcases the strategic motivations behind cross-border deals. These variations highlight the influence of regional economic climates, sector-specific strengths, and valuation expectations. For instance, the DACH region exhibits higher multiples in the software development sector at 8.5x, yet it shows significantly lower multiples in the retail trade sector at 2.8x.

In contrast, France boasts higher multiples in the Media & Communication sector at 4.9x, with its other sectors aligning closely with average values compared to its peers. Meanwhile, the Netherlands shines in the Wholesale trade sector with a 5.3x multiple but presents lower multiples compared to the broader Western Europe landscape.

This emerging trend not only underscores the interconnectedness of global markets but also illuminates the arbitrage opportunities that investors and corporations are eager to exploit, whether through acquiring a foreign company or selling to an international buyer.

The shifting landscape of M&A financing and deal structures

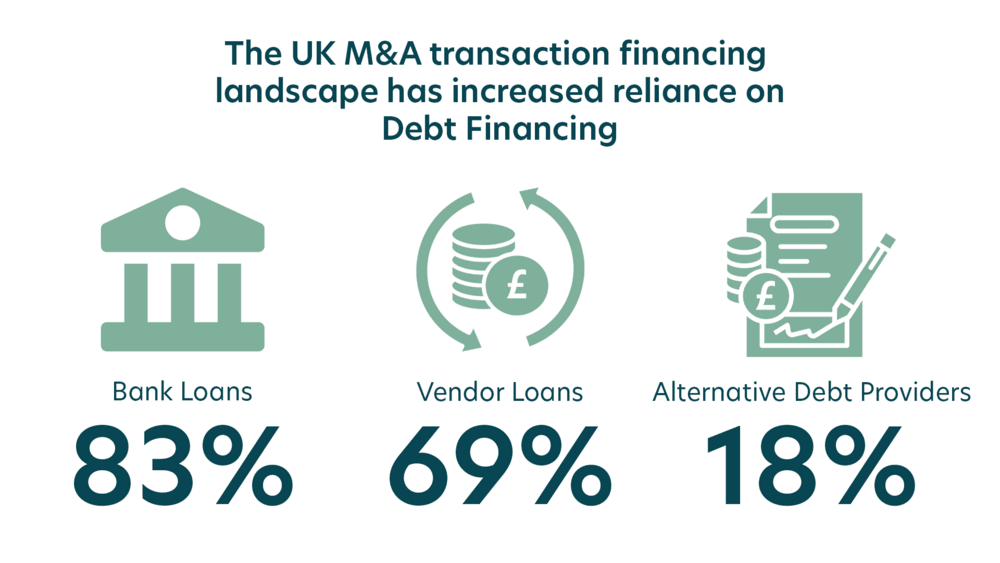

The M&A transaction financing landscape has undergone a nuanced yet impactful transformation, with an increased reliance on debt financing, escalating from 35% in the first half to 43% in the second half of the year, alongside an average debt capital contribution to total transaction value standing at 49%. This shift, coupled with the diverse mix of financing sources including bank loans (utilised in 83% of transactions involving debt financing), vendor loans (in 69% of such transactions), and alternative debt providers (in 18% of transactions involving debt financing), reflects the strategic financial adaptations companies are making to thrive in an era of elevated interest rates.

Furthermore, the development of deal structures, especially the complex aspects of earn-out arrangements, indicates a market striving for a balance between risk and potential rewards. Earn-out mechanisms aim to maintain seller involvement post-transaction to ensure the company's performance, which in turn, affects the final payout.

From 2020 to the latter half of 2023, the occurrence of earn-outs in debt-financed transactions slightly rose from 40% to 42%. Simultaneously, the average duration of these agreements reduced from 28 to 23 months. Earn-outs now represent a smaller segment of the total deal value, having decreased from 38% in the first half of 2020 to 29% by the second half of 2023, indicating a shift in the market towards smoother transitions and more closely aligned interests between buyers and sellers.

Looking ahead

The prevailing optimism for the first half of 2024, with 77% of advisors expressing a positive outlook, stands as a compelling testament to the anticipated direction of the market. In the face of existing challenges, this forward-thinking sentiment highlights a widespread conviction in the strength and future prospects of the UK&I M&A sector.

As we pivot towards the future, the lessons of adaptability, strategic foresight, and resilience from H2-2023 will undoubtedly serve as guiding principles.

In conclusion

The insights gained from the H2-2023 M&A Monitor highlight a resilient and optimistic market, adept at steering through periods of instability. At GS Verde Group, these insights align closely with our perspective and future expectations for the M&A sector.

As an agile, multidiscipline firm, we are dedicated to utilising our deep-rooted expertise to navigate our clients through the multifaceted challenges and prospects this setting unveils.

GS Verde Group’s multidiscipline team combines law, finance, tax, and communications to provide all the support needed for M&A transactions nationwide. Helping business owners to Buy, Sell, or Raise - they are the business-focused experts in getting deals done, providing a truly holistic, end-to-end service to achieve the most optimal outcomes for businesses across the UK & Ireland.